Introduction

The Coalition for Better Housing is a broad-based, non-profit organization made up of individuals and organizations committed to meeting San Francisco's need for more and better housing. Adamantly opposed to rent control for San Francisco, responsible housing industry leaders active in the Coalition's work, have censored the few landlords who have levied unfair rent increases and refused to pass on Prop. 13 savings to their tenants.

Members of the Coalition for Better Housing believe San Francisco can meet its citizens' housing needs without imposing the disastrous economic and social effects brought on by rent controls wherever ney Wceie been tried. Coalition programs include:

- Maintaining an information/resource center of materials on housing with an emphasis on San Francisco data.

- Conducting market research and resident attitude surveys in order to gather accurate information on rent rebates, rent increases, owner/renter relations, quality of units, and other pertinent information.

- Working with community renters and owners to identify the legitimate concerns of each group to produce positive solutions.

- Encouraging dialogue between those with housing concerns and government officials in order to facilitate responsive and accountable action.

- Monitoring legislation, particularly at the City level, to ensure equitable and appropriate housing policy.

- Communicating housing information with an emphasis on neighborhood interests to City residents, and

- Informing Coalition members about San Francisco housing issues.

The Coalition for Better Housing has endorsed the San Francisco Planning and Urban Research Association Report on housing and recommend it to the community. Recently, numerous radio and television programs have featured Coalition members' considerable expertise on how San Francisco can increase its housing stock, the only rational means of serving its citizens' varied housing needs. To that end; the measures outlined below; are offered for consideration.

NEEDED: A Comprehensive Housing Program for San Francisco.

San Francisco must have a Comprehensive Housing Program with policies and action :guidelines for short-term and long-term housing improvement. Much of the background work for such a Program has already been completed. It should now be a priority for City officials to establish housing goals and objectives, by type, and to cut through existing obstacles which prevent implementation.

San Francisco has the human and monetary resources available to provide housing assistance to its citizenry. Other cities have tried and failed to meet complex housing problems; those which have resorted to rent controls have only exacerbated their problems.

The citizens of San Francisco are currently plagued by across the board double-digit inflation. A consistently low vacancy rate of two to three percent over the past five years, rising land and construction costs, lengthy bureaucratic delays which discourage development of badly needed new units, added to the desirability of living in this City, present a challenge to meet current housing demands.

Members of the Coalition for Better Housing stand ready to actively participate in all constructive efforts to develop and implement a Comprehensive Housing Program, and encourage the entire community to contribute to enhancing and building this fine City.

NEEDED: Renter Relief

Nearly 70 percent of San Francisco's residents are renters, which is double the national average. Of the 315,000 dwelling units in the City, two-thirds of the units are rentals; one-third are owner occupied. Rents in most San Francisco buildings have not kept pace with inflation or with the spiraling costs of home ownership. In order to provide as much rent relief as possible, CBH supports the following measures:

- State Senator Milton Marks, (R. San Francisco) has legislation pending which would increase the present $37 credit each renter or married renter couple can claim, to a higher amount which would be established according to a sliding scale of income. Senator Bob Wilson, (D. San Diego) also proposed a bill which received Senate approval to make the credit a flat $137 per household no matter how many income taxpayers lived under the same roof. Both bills are before the Senate Finance Committee.

- Mayor Dianne Feinstein's recently proposed Rental Affairs Bureau for mediation and housing information dissemination will be a valuable City-service.

- San Francisco must consider tying the number or new office spaces, estimated to be 13 nit Mallen square feet of already approved space to be built by 1985, to affordable housing for office workers and support staff.

- Revitalization of neighborhoods, a more acceptable approach than redevelopment given our present housing shortage and the time it takes to replace units, must be a priority. The use of Community Development Block Grants should be encouraged so that existing units remain a vital part of the housing ladder. Tax abatement programs and other financial incentives for maintaining older units should also be explored and used to the greatest extent possible (see Appendix for federal and state programs).

- When the City is involved in financing rehabilitation of existing units and construction of new rental units, it should adopt a program to minimize construction costs by the use of standardized building techniques and materials so that savings can be passed on to renters. A lottery should be established to choose between the many people who will want to live in these low and moderatety priced units.

- Programs such as the one being considered in Nashville, Tennessee, to subsidize the interest on rehabilitation of rental property using CDBG funds, should be considered.

NEEDED: A Condominium Ordinance

The American dream of home ownership can often only be realized by 'purchasing a condominium. New condominiums and converted units are in high demand in San Francisco today, as they present a way to: hedge against rising housing costs for those who wish to remain in the City. These purchases offer the opportunity to pay off loans with cheaper money over time, rather than pay increasing Condominiums make up only. one percent of the housing stock in San Francisco today, but will present a very good investment for middle-income people who cannot afford single family homes or owning entire apartment buildings.

CBH supports a progressive condominium ordinance with life-time leases for senior citizens. It makes sense that gains in real estate values should go to the occupant rather than to a landlord. The prices of condominiums should stabilize or decline when more units are on the market. These prices have been kept artificially high by the political restrictions on conversions.

San Francisco must not force people to rent housing rather than receive home ownership benefits by political intervention into a market which demands more home and condominium ownership opportunities and a stable City population,

NEEDED: Investment Capital and Construction Incentives

Many Federal and state financing programs exist which can be more fully utilized in San Francisco housing construction (see Appendix).

CBH calls on the City to establish a tax-exempt bond program to provide mortgage loans below market rates for middle and lower income people so that they can accrue ownership benefits.

New credit and appraisal guidelines announced by the Federal Home Loan Mortgage Corp. could make it easier for thousands of Americans to purchase homes.

The proposed changes include:

Raising the percent of gross monthy income families can spend on mortgage payments, insurance and taxes to between 25 and 28 percent;

Increasing the allowable debt payments a family can have and still qualify to range between 33 and 36 percent;

Considerations of age, race or religion of borrowers and the location of the property they wish to purchase will not be of prime concern in the future; and

The expected "economic life" of the property will not be considered relevant unless it is five years or less.

San Francisco should support these new guidelines which were designed to overcome discrimination against inner-city neighborhoods, minority borrowers, and older homebuyers.

CBH calls on the City to support the Graduated Payment Mortgage legislation now-before both houses of Congress. The GPM, which now accounts for one in every four Toans insured by the FHA, would allow borrowers to maintain low, initial monthly payments for the first several years; payments would increase at a rate of four or six percent over the next ten years before leveling off for the remainder of the loan. It also provides for lower down payments.

This program would provide young buyers with the boost they need to qualify for loans. °- As their earnings increase, they can afford to put more of their income into housing payments. The Housing Opportunity Act speaks to the needs of many young San eee who plan to call the City home for some time to come.

The Coalition surveyed cities across the country struggling with housing production and found the following:

In Albuquerque, New Mexico, officials encourage single family home purchases with a tax exempt bond plan called the Single Family Mortgage Purchase Program.

Des Moines, Iowa, has legislation pending in the Iowa State Legislature called the Urban Revitalization Bill which would allow cities to use tax exemptions and mortgage bonds to encourage housing rehabilitation and new construction within designated areas.

More than a hundred units of elderly housing have been constructed recently in Billings, Montana with first mortgage revenue bonds. City taxes for elderly homeowners are also deferred in Billings.

Indianapolis; Indiana, uses tax exempt bonds and also has ere tax abatement programs which pro- vide incentives for building multi-family housing. These programs recognize the importance of private participation investment capital and job creation. They provide private developers with incentives in the form of reduced property taxes on increased assessment due to either new construction or rehabilitation prpjects in designated areas. In Indianapolis, this incentive has been responsible for more than 24 1/2 million dollars of new construction and has created 1300 new jobs , Since January 1978. The tax abatement on buildings -- not land -- is 100 percent for the first year and is reduced to 50 percent in the fifth year.

In Charleston, South Carolina, $100,000 in Community Development funds has been used to write down the interest on loans to homeowners. This program, which is in the formative stages, should enable people to purchase homes at an interest rate reduced by two to three percent. Charleston also actively participates in the 312 program which awards loans for rehabilitation at three percent for 20 years. These loans are available to CDBG target areas and the maximum is $27,000.

Charleston was awarded a special Section 8 grant for rehabilitation through the Neighborhood Strategy Area program, and will be using 312 funds as the financing mechanism for this program whenever possible. Low interest loan grant programs for target areas are also available throughout the city.

Kansas City, Missouri, under tax abatement and the power of eminent domain to private developers working in blighted areas, has realized new multiple housing units for persons in the middle and upper income ranges. The Missouri Housing Development Commission, the State's housing finance agency, is involved in financing the construction of several subsidized housing projects in Kansas City. The Commission has a mortgage purchase program that enables moderate-income home buyers to purchase housing for slightly below market interest rates.

Kansas City officials have been working with home builder associations to improve the climate for development in the city, including a fast-track option for developers who need to minimize the time it takes to get through the City processes. A suburban type subdivision, Kensington Place, is being built in the inner city. It is 100 single family units with prices ranging from $60,000 to $100,000. Community Development Block Grant funds were used to provide public improvements such as streets and curbs. All of these programs have added up to Kansas City leading the region in building permits and new construction activity.

Land packaging and writing down costs to encourage development in blighted areas has also been successful in many cities concerned about rehabilitation and new construction. Fee waivers have been granted to developers willing to rehabilitate rundown housing.

Tax abatement programs such as Kansas City, Kansas, uses, encourage private redevelopment corporations to tackle hard-core blight. The program in Kansas City on urban redevelopment runs for 25 years: full abatement for ten years; 50 percent abatement on land and improvements for the remaining 15 years.

San Francisco must seek additional Section 8 money, SB 99 funding, and every avenue if housing is to be built in this City.

A comprehensive Housing Program for San Francisco would develop yearly Housing Action Goals and make full use of the Housing Opportunity Sites Report, recently developed by City planners. Members of the Coalition for Better Housing urge City officials to work closely with State and Federal agencies, as well as private business, industry, and community interests to ensure that every possible housing opportunity is realized in a timely fashion.

NEEDED: A Stremlined Permit Process

It is essential that San Francisco revamp its present permit process which causes costly delays resulting in increased costs for builders and ultimately owners and renters. The present lock-step method of achieving each necessary requirement is unacceptable in terms of time which equates to money. Between 10 and 12 percent could be saved on housing if a fast-tracking permit system were implemented.

Many of the necessary tasks can be accomplished simultaneously with proper organization, thus aiding the cause of affordable housing.

In Phoenix, Arizona, new housing costs are being lowered by speeding up processing time of permits and rezoning cases and other development reviews such as abandonments. They have achieved this by using administrative staff sign offs rather than formal Commission, Board or Council action on the more routine matters.

NEEDED: Zoning Modifications

With minor modifications in present zoning ordinances and by using variances, many additional housing units could be realized which would be consistent with the Design Controls for the City. These modifications should take into account transportation corridors, parks and recreations facilities available for increased population, and the like. An example: Corner lots often have buildings which could easily accommodate additional units without disrupting the neighborhood. A realistic density policy for each neighborhood would aid in taking advantage of these slight modifications which would add up to more rental units so badly needed at this time.

Improved procedures need to be worked out for conditional use permits on code restricted sites when appropriate.

A close examination of building codes should be made with present needs in mind and an awareness of new construction methods and more efficient uses of materials.

NEEDED: Public and Private Land Suitable for Building New Units

A thorough inventory of available construction sites 'has been made by the City Planning Department. CBH urges the City to develop a system of priorities on housing according to need and in accordance with the spirit of downzoning which was to preserve and enhance neighborhoods, and then do everything in its power to make new housing construction possible on these sites to meet yearly goals.. Realizing these 40,000 units would help San Francisco avoid future housing crises, and each increment will produce a healthier housing market for today's citizen

San Diego, California, has a unique city-sponsored land-lease program to stimulate the construction of needed low-income housing. The city makes surplus land available at minimal costs to private and non-profit developers if they can produce apartments with reasonable rents. Almost 500 units for low income residents -- mostly elderly -- have been completed, and 2,000 units are planned: using this method.

Faced with a threat by the U.S. Department. of Housing and Urban Development to cut off $31 million in grants, the San Diego City Council recently approved applications for federal funds to build or buy 1,058 units for low-income families and persons. It wiil per thie first time San Diego has had an actual housing authority. Peter Wilson, Mayor of San Diego isn't a proponent of counting on the federal dollar alone and has clearly made.known his preference for using city land to encourage private development of low-cost housing.

His reasons include the speed with which those units can be delivered, the return of public lands to the tax roles, and the flexibility of being able to use federal rent subsidies. The land leases run for 50 years.

In a rare display of bureaucratic initiative, San Diego, cut costly delays for developers who have to file cumbersome environmental impact reports and requests for zoning variance, by having the city administration take care of these steps before offering the land for these long-term Jeases.

In San Francisco, public schools which have been abandoned, provide a chance to house more people in residential areas. If, as rumored, the Army leaves San Francisco, the Presidio is a prime site for rehabilitated housing while maintaining the existing open space as a nature preserve and recreation area. The South of Market/China Basin area could become a very attractive residential area serving downtown workers. Numerous opportunities will undoubtedly present themselves once housing is established as a priority.

NEEDED: Planning Commission Accountability

The Planning Commission has the leadership responsibility and the means by virtue of present downzoning ordinances, design controls, and other regulations, to ensure not only more housing units, but a liveable environment. The Coalition for Better Housing suggests that there are sufficient laws and regulations on the books at this time to achieve these purposes. In many respects, the present perceived housing crisis has been brought on in part by the insensitivity of elected and appointed officials to the need for more housing in San Francisco for the past several years.

San Francisco is a vital city with creative, industrious people. The challenge is to use the 'available good will and energy to solve the problems which exist.

Urban Neighborhood Community Associations, cooperative housing ventures, the use of sweat equity in producing housing, are only a few possibilities which can be drawn on to achieve housing for people.

The Coalition for Better Housing supports measures which will increase San Francisco's housing supply, maintain and enhance existing neighborhoods, and add to the general well being of the City. The imposition of rent control, a brief and ultimately costly means of relief for a few, is not the answer to present complex economic and social issues. Too many options exist and too many resources are available to impose such a measure on this City which has had devastating--effects on cities -across the country.

San Francisco deserves better -- housing, not rent control.

APPENDIX

1. Federal Programs

a. Section 23 (Low=Rent Public Housing)

Description

Section 23 of the U.S. Housing Act of 1937, as amended, authorizes local housing authorities to lease existing vacant dwelling units from the private market for low-income families. These units may be leased for periods of up to five years. Funds are received for the operation of the program by entering into an annual contribution, the housing authority pays the property owner the difference between what the low-income tenant can afford to pay (a maximum of 25% of gross income) and fair market rent. Units of any size or type (apartments or detached single-family) may be utitlized in accordance with the Annual Contributions Contract and by its very nature, the program allows for the dispersal of assisted housing. Originally scheduled for termination in June of 1978, the program has been extended to September 30, 1979. Consideration is being given in Washington to an indefinite extension of the program.

b. Section 221 (d) 3

Description

The first below-market interest rate program, Section 221 (d) 3 of the National Housing Act, was enacted in 1961. It authorized the insurance of long term, low interest (3% set in 1965) mortgage loans on inexpensive rental housing. Sponsorship of the housing was limited to non-profit, limited dividend, and cooperative associations. Even with a 40-year, 3 percent mortgage, sponsors were not able to produce housing for low-income families, because of the gap between tenant income and the cost of housing. To reach low-income families, Congress in 1965 authorized the FHA to make annual rent supplement payments on behalf of qualified tenants of non-profit, limited dividend, or cooperative owners of rental housing projects insured under Section 221 (d) 3. Some of the 221 (d) 3 projects receive these rent supplement payments.

c. Section 236

Description

Section 236 represented an extension of the Section 221 (d) 3 below-market interest rate program. Instead of the 3 percent authorized under Section 221 (d) 3, Section 236 authorized a market interest rate with periodic assistance payments made to the lender on behalf of qualified tenants to reduce the interest paid by the owner to not less than 1 percent. Tenants, to be eligible for initial occupancy, must have adjusted incomes not exceeding 80 percent of the area's median income, except that HUD may allow increases in the income limits on a project-by-project basis under certain circumstances. The tenants in particular projects can receive rent supplements or public housing assistance under the Section 23 leasing program or the Section 8 (Existing) program.

d. Section 235

Description

Section 235 was added to the National Housing Act by the Housing and Urban Development Act of 1968. Section 235 (i) authorized mortgage insurance: forhomes of low-income purchasers, but not for project mortgages. It provided for insurance of mortgages involving: (1) single-family dwelling units approved prior to construction or substantial rehabilitation; and (2) individual units in existing projects covered by mortgages insured under Section 236 or individual units in existing projects receiving rent supplement assistance. Depending on the purchaser's income, the insured mortgage could be subsidized to the extent that the purchaser would only pay 1% interest.

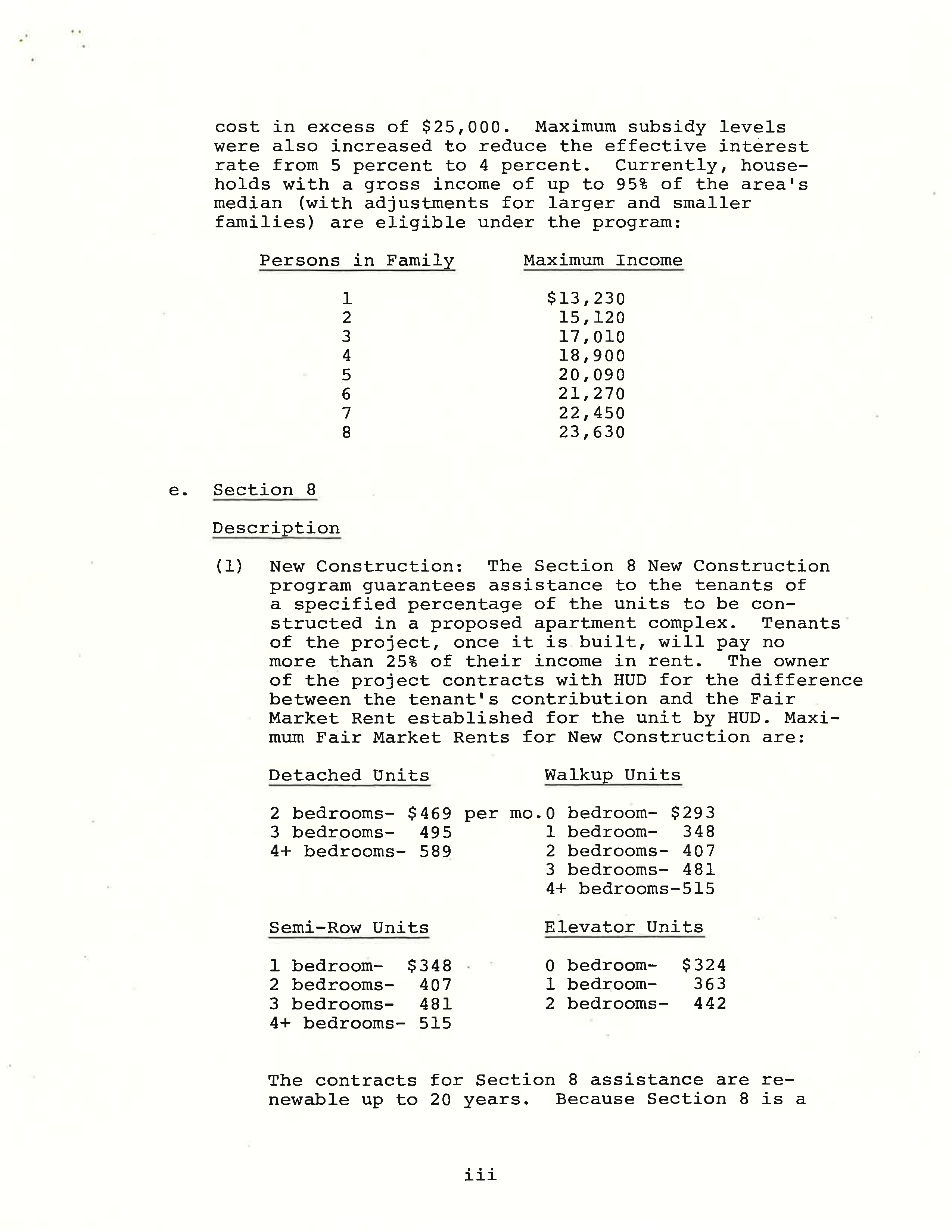

The funds for the 235 program were impounded in 1973. The program was reactivated in January, 1976, but the- assistance offered was considerably different than under the original program. The interest subsidy was less than the original program provided and the down payment requirement was greater. Also, "existing" units no longer qualified for financing under the program.

Regulation changes in:1978 provided for reduction of the minumum downpayment to 3 percent of the cost of acquisition instead of 3 percent of the acquisition cost in excess of $25,000. Maximum subsidy levels were also increased to reduce the effective interest rate from 5 percent to 4 percent. Currently, households with a gross income of up to 95% of the area's median (with adjustments for larger and smaller families) are eligible under the program:

Persons in Family Maximum Income

1 $13,230

2 15,120

3 17,010

4 18,900

5 20,090

6 21,270

7 22,450

8 23,630

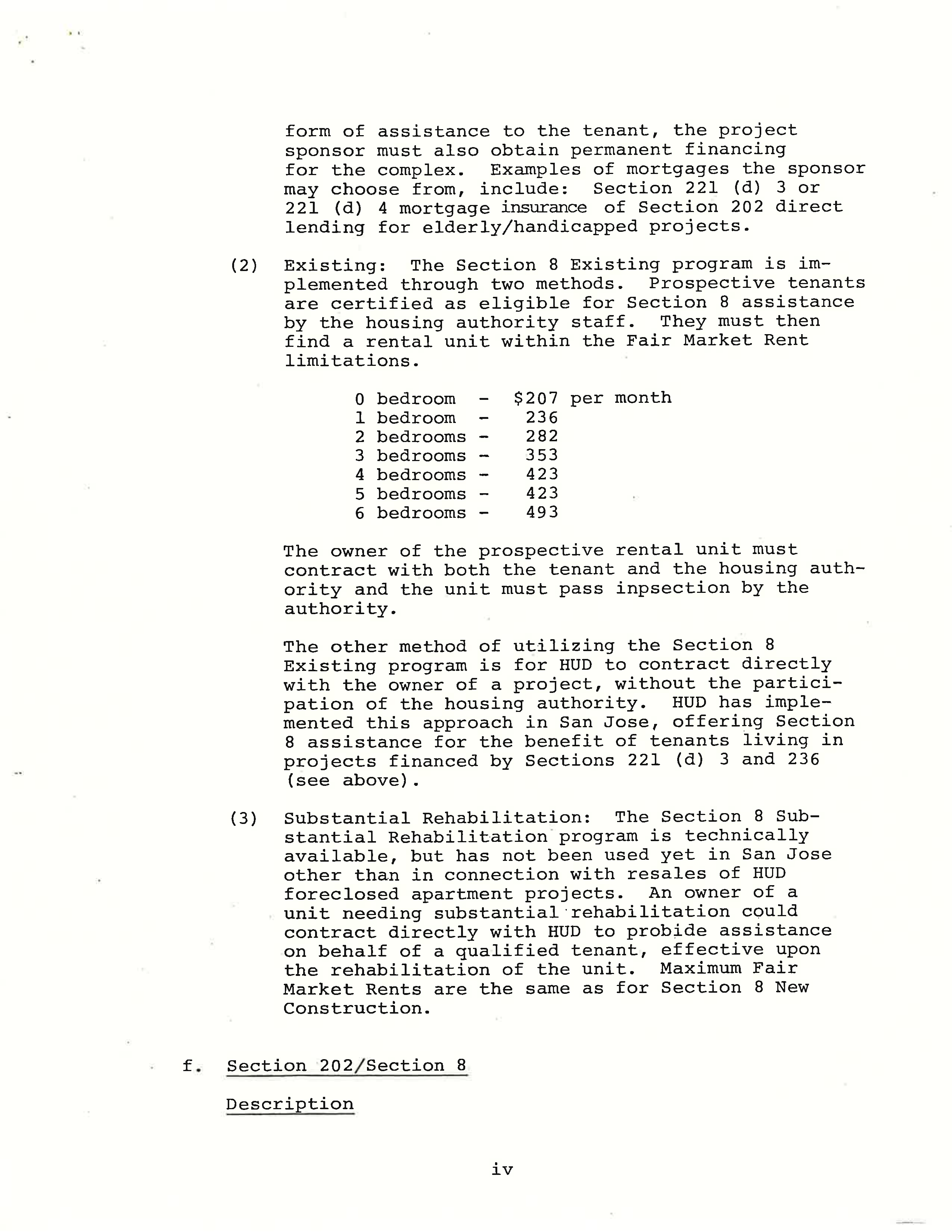

e. Section 8

Description

(1) New Construction: The Section 8 New Construction program guarantees assistance to the tenants of a specified percentage of the units to be constructed in a proposed apartment complex. Tenants of the project, once it is built, will pay no more than 25% of their income in rent. The owner of the project contracts with HUD for the difference between the tenant's contribution and the Fair Market Rent established for the unit by HUD. Maximum Fair Market Rents for New Construction are:

Detached Units:

- 2 bedrooms- $469 per mo.

- 3 bedrooms- 495

- 4+ bedrooms- 589

Walkup Units:

- 0 bedroom- $293

- 1 bedroom- 348

- 2 bedrooms- 407

- 3 bedrooms~ 481

- 4+ bedrooms-515

Semi-Row Units:

- 1 bedroom- $348

- 2 bedrooms- 407

- 3 bedrooms- 481

- 4+ bedrooms- 515

Elevator Units:

- 0 bedroom- $324

- 1 bedroom- 363

- 2 bedrooms-— 442

The contracts for Section 8 assistance are renewable up to 20 years. Because Section 8 is a form of assistance to the tenant, the project sponsor must also obtain permanent financing for the complex. Examples of mortgages the sponsor may choose from, include: Section 221 (d) 3 or 221 (d) 4 mortgage insurance of Section 202 direct lending for elderly/handicapped projects.

(2) Existing: The Section 8 Existing program is implemented through two methods. Prospective tenants are certified as eligible for Section 8 assistance by the housing authority staff. They must then find a rental unit within the Fair Market Rent limitations.

- 0 bedroom - $207 per month

- 1 bedroom - 236

- 2 bedrooms - 282

- 3 bedrooms - 353

- 4 bedrooms - 423

- 5 bedrooms - 423

- 6 bedrooms - 493

The owner of the prospective rental unit must contract with both the tenant and the housing authority and the unit must pass inpsection by the authority.

The other method of utilizing the Section 8 Existing program is for HUD to contract directly with the owner of a project, without the participation of the housing authority. HUD has implemented this approach in San Jose, offering Section 8 assistance for the benefit of tenants living in projects financed by Sections 221 (d) 3 and 236 (see above).

(3) Substantial Rehabilitation: The Section 8 Substantial Rehabilitation program is technically available, but has not been used yet in San Jose other than in connection with resales of HUD foreclosed apartment projects. An owner of a unit needing substantial rehabilitation could contract directly with HUD to probide assistance on behalf of a qualified tenant, effective upon the rehabilitation of the unit. Maximum Fair Market Rents are the same as for Section 8 New Construction.

f. Section 202/Section 8

Description

The Section 202 program provides housing and realted facilities for the elderly or handicappped. HUD makes long term direct loans to eligible, private, nonprofit sponsors for new construction or rehabilitation of rental or cooperative housing facilities for elderly or handicapped persons. Single and multi-family structures are eligible. The current interest rate is based on the average U.S. Treasury borrowing rate during financing, sponsors also receive a set-aside of Section 8 housing assistance to subsidize on-going operations.

g. Section 312

Description

This program offers direct 3% rehabilitation loans from HUD to owners of dwelling units needing repairs. The loan term is up to 20 years and the maximum loan amount is $27,000. In some circumstances, these loans may refinance existing debt on the property. These loans are only available in CDBG Target Areas.

2. State Programs

a. California Housing Finance Agency (CHFA) PMI/FHA/VA Insured Home Ownership and Home Improvement Program

Description

CHFA guidelines originally places no income limitation on borrowers who purchased dwellings in CRA's. However, contemplated rule-changes will make these loans in CRA's available only to below moderate income families and investors. For loans to purchase one unit structure must have been vacant and for sale for at least 90 days prior to making application for a loan. When investor borrowers purchase 2-4 units, this 90-day requirement is invalid, but they must have a relocation certificate signed off by the particular locality.

If the purchaser.wishes . to rehabilitate the unit, the mortgage amount will be calculated from the "after improved rehabbed value." Maximum sales price limits for 2 through 4 unit is.$69,000, plus specified amounts based upon the number of bedrooms in each unit.

b. CHFA Title I Home Improvement Loan Program

Description

The California Housing Finance Agency has contracted with Security Pacific Bank to originate FHA-insured Title I Home Improvement loans. The program applies to one to four unit structures which the borrower must have owned for at least one year. For single family homes, the maximum loan amount if $15,000 for a maximum term of 15 years. Two to four unit dwellings are eligible for $5,000 per unit for no longer than 12 years. The interest rate on these loans was 9% as of December, 1978. For owners of property inside the City's four concentrated rehabilitation areas (Northside, Gardner, Olinder, Mayfair), loans may be made without regard to income or occupancy status. If the property is outside the CRA. the borrower's income must fall below the moderate income level as defined in CHFA's Home Ownership and Home Improvement Program and the property must be single family (one unit) and owner occupied. Rehabilitation work is limited to code violations and a limited amount of general improvements.

c. Cal-Vet Home Loans

Description

Veterans born in California, or who were residents of California at the time of enlistment may be eligible for 5.6% financing of owner-occupied units. Only those veterans who served during certain time periods are eligible. The 5.6% loans are not backed by mortgages; rather, the veteran buys the house on a contract of maximum loan amount if $43,000 or 95% of the value of the property, whichever is less. The terms of the loans are generally 25 years. Newly constructed, standard existing and substantially rehabilitated units are all eligible for financing under this program.

d. Cal-Vet Home Improvement Loans

Description

Those veterans already purchasing a home under the Cal-Vet program are also eligible for additional loans to finance reahbilitation. Loans of up to $10,000 for terms of up to 10 years are available, to the extent that the total indebtedness on the property does not exceed $43,000. The interest rate on these loans is also 5.6%.